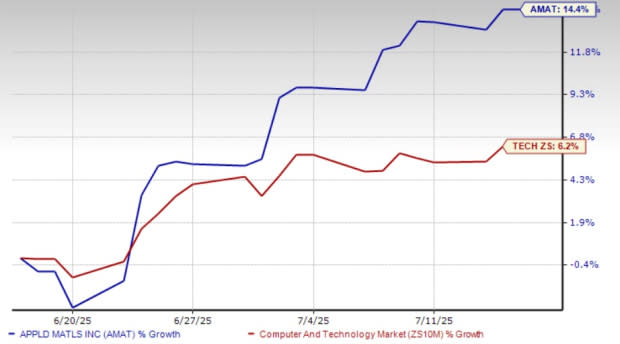

Applied Materials AMAT shares have climbed 14.4% in a month, outperforming the Zacks Electronics - Semiconductors industry’s return of 6.2%. This outperformance raises the question: Should investors accumulate AMAT shares or book profits and exit the investment?

Applied Materials One Month Price Performance Chart

Zacks Investment Research

Zacks Investment Research

Image Source: Zacks Investment Research

AMAT Benefits From Growing Adoption of Its Products

Applied Materials is experiencing strong traction in its etching, deposition, metrology and inspection tools. AMAT’s Sym3 Magnum etch system, Cold Field Emission eBeam technology, gate-all-around, backside power delivery, and 3D DRAM technology nodes are gaining traction as they play crucial roles in the manufacturing and inspection of high-performance processing and memory chips used for AI and HPC workloads.

AMAT’s Sym3 Magnum etch system has yielded more than $1.2 billion in revenues since its launch in February 2024. Moreover, in the second quarter of fiscal 2025, AMAT’s management anticipated AMAT's revenues from DRAM customers to grow more than 40% in fiscal 2025. Earlier, Applied Materials reported that its revenues from advanced semiconductor nodes crossed $2.5 billion in 2024, and it expected the figure to double in fiscal 2025 as customers’ adoption of its GAA and backside power delivery solutions grows.

Applied Materials stands to gain from the rising demand for advanced chips required to power AI-centric data centers. The company's deep expertise in logic and solid position in DRAM patterning have aided it in maintaining a stronghold in the semiconductor space. Its patterning systems and technologies, which are designed to address the shrinking pattern dimension challenges and the growing complexity in vertical stacking, can play a crucial role in high-performance chip development for AI.

Due to the favorable mix of products and traction in high-margin solutions, Applied Materials’ gross margin has been experiencing positive momentum for the past four quarters and came in at 49.2% in the second quarter of fiscal 2025, which is also the highest gross margin since the fourth quarter of fiscal 2000.

Broad Portfolio Gives AMAT a Competitive Edge

The semiconductor equipment market in which AMAT operates has other larger players, including Lam Research LRCX, ASML Holding ASML and KLA Corporation KLAC. However, AMAT differentiates from its competitors by providing comprehensive deposition, etch, metrology, and packaging solutions, whereas its competitors specialize only in one vertical or the other. AMAT also commands a strong integration of materials science and fabrication; the others don't.

繼續閱讀For instance, ASML Holding specializes in the photolithography and advanced manufacturing equipment segment. KLA Corporation is a dominant competitor in the wafer inspection space and Lam Research has a strong atomic layer deposition portfolio. AMAT stands out because of its full-stack portfolio, strength in materials engineering, and ability to co-optimize across fabrication steps.

This is the reason why, despite having competition from Lam Research, KLA Corporation and ASML Holdings, Applied Materials is able to keep its margins intact as it’s not just a tools vendor. Applied Materials offers end-to-end solutions that improve chip yield, power, performance, and cost. The Zacks Consensus Estimate for AMAT’s earnings per share is pegged at $9.47, indicating year-over-year growth of 9.5%.

Zacks Investment Research

Image Source: Zacks Investment Research

Applied Materials is trading at a 12-month forward P/S ratio of 5.34, significantly below the industry average of 6.64. Given its dominance in semiconductor equipment and AI-driven chip manufacturing, this valuation discount suggests strong upside potential over the long term.

AMAT Forward 12 Month (P/S) Valuation Chart

Zacks Investment Research

Image Source: Zacks Investment Research

Conclusion: Buy AMAT Stock Now

Applied Materials remains a key player in semiconductor manufacturing, with a strong position in AI-driven chip development, advanced packaging and next-generation process technology. For investors, investing in AMAT stock remains the best approach. Currently, Applied Materials carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

KLA Corporation (KLAC) : Free Stock Analysis Report

ASML Holding N.V. (ASML) : Free Stock Analysis Report

Lam Research Corporation (LRCX) : Free Stock Analysis Report

Applied Materials, Inc. (AMAT) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research